|

|

|

|

|

|

|

|

|

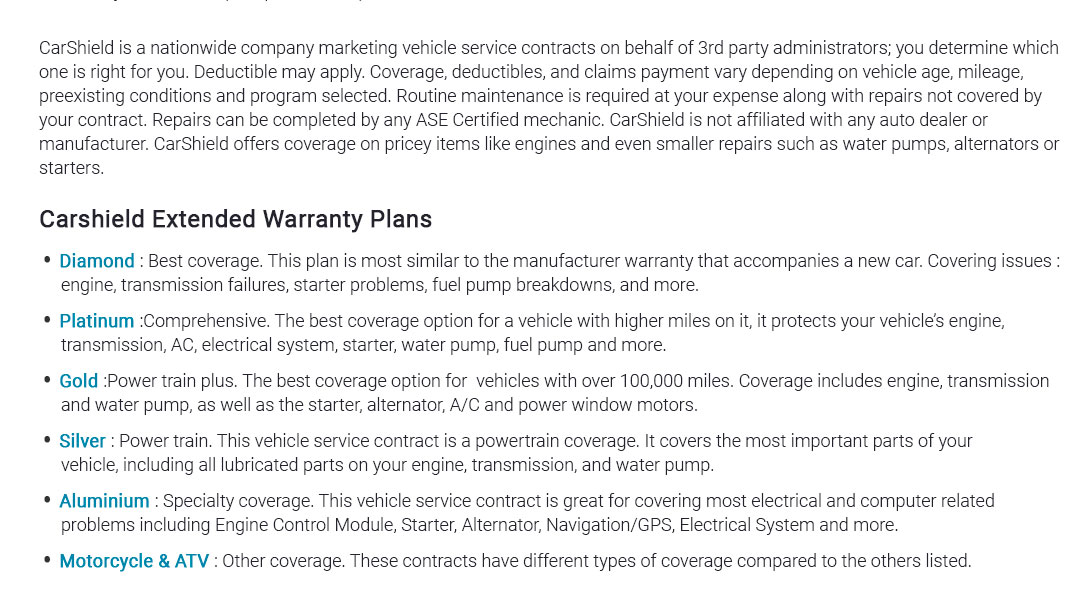

|||

|

|

|

|||||||

|

|||||||

|

|||||||

|

|||||||

|

|||||||

|

|||||||

|

||||||

|

||||||

|

||||||

|

||||||

|

|

|

|

|

|

|

|

extended car warranty policies explained for confident decisionsClear coverage. Predictable costs. Fewer surprises. That is the point. Core ideaAn extended policy is a service contract that steps in after the factory warranty ends or alongside it for specific components. It converts uncertain repair risk into a planned payment. Trust grows when the terms are plain and the process is repeatable. Result: the car gets fixed, you keep moving. Coverage anatomy

Coverage tiers

What is not covered

Costs and math

Small pause: read the sample contract once. Quietly note definitions. Workflow: selection

Using the policyFollow the process; it keeps approvals fast.

Real moment: the starter clicks on a cold Monday. You hand the service writer your policy card; they call, claim authorized, new starter installed by lunch. Back to work. Trust signals

Edge cases and tips

Compare options, then decideIf it fits your plan, compare an OEM-backed contract, a third-party administrator policy, and any credit union offerings. Match term to how long you will keep the car, not how long you might. Quick checklist

Keep it simple. Choose for trust. Measure by result. https://www.cars.com/car-warranty/money/best-extended-car-warranty-plans/

What Does an Extended Warranty Cover on a Car? Generally, extended warranties cover mechanical breakdowns and failures that occur due to normal ... https://www.edmunds.com/auto-warranty/understanding-extended-warranties.html

An extended warranty is actually an insurance policy on your vehicle, a safeguard against expensive, unforeseen repairs. https://www.cartalk.com/extended-warranties/understanding-extended-warranty-laws-state-by-state-guide

Extended warranties must, at minimum, be returnable at any time for a pro-rated refund, minus any claims paid and at most, a 10% administrative ...

|